Understanding Rare Earth Elements: Strategic Metals at the Heart of Global Competition

Over the past two weeks, I’ve been researching a promising small-cap stock that stands to gain from the growing spotlight on Rare Earth Elements — a sector quickly becoming one of the most strategically important in the world.

In this article, I’ll walk you through everything you need to know about the REE landscape: what makes it so critical, the global imbalance that threatens supply chains, and — most importantly — the key challenge that needs solving.

Make sure to subscribe, because a full Deep Dive on the company I’ve been researching is coming soon.

What Are Rare Earth Elements (REEs)?

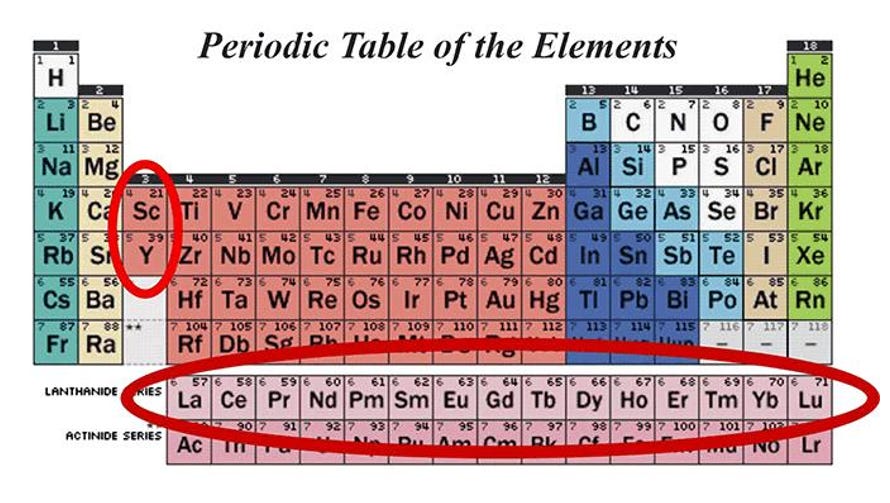

Despite the name, REEs are not geologically rare. The term refers to a group of 17 chemically similar elements: the 15 lanthanides (atomic numbers 57–71) plus scandium and yttrium. These elements typically occur together in mineral deposits, making their separation and extraction complex and resource-intensive.

Since their discovery in the late 18th century — starting with yttrium, named after the Swedish village of Ytterby — REEs have gradually become integral to modern life. They enable critical functionality in technologies such as smartphones, electric vehicles, wind turbines, medical imaging devices, advanced defense systems, robotics, and more.

Because of their unique magnetic, luminescent, and electrochemical properties, REEs are often described as the “vitamins” of modern industry.

Why Rare Earths Matter

REEs are foundational to the technologies that define the 21st-century economy and global security landscape. From decarbonizing energy systems to building autonomous weapons and intelligent machines, REEs are indispensable to innovation, infrastructure, and sovereignty.

Powering the Clean Energy Revolution

As nations pursue aggressive climate goals, REEs are increasingly recognized as non-substitutable components in technologies driving the energy transition:

Neodymium and dysprosium are used to create high-performance permanent magnets in EV motors, wind turbines, and hydrogen fuel cells. These magnets deliver exceptional strength in compact formats, allowing for lighter, more efficient, and longer-lasting systems.

Lanthanum and cerium are essential in automotive catalytic converters, battery electrodes, and energy-efficient lighting — technologies that reduce emissions and improve fuel economy.

Europium, terbium, and yttrium are critical in phosphors that illuminate LED screens, television displays, and medical imaging systems, offering not just efficiency but also clarity and precision in visualization technologies.

In short, REEs are at the heart of the global shift toward cleaner, smarter, and more resilient energy systems.

Enabling Robotics, AI, and Automation

The rise of robotics and artificial intelligence adds another layer to the strategic importance of rare earths. These technologies rely on advanced electromechanical components, high-speed data processing, and sensor fusion systems — all of which depend on rare earth-enabled materials.

Permanent magnets made from neodymium, dysprosium, and praseodymium are critical in robotic actuators and motors, which drive movement in industrial robots, drones, surgical robotics, and autonomous vehicles. Without these lightweight, high-efficiency magnets, the precision and dexterity of modern robots would be severely limited.

High-performance sensors, such as those used in LiDAR systems, machine vision, and real-time environmental mapping, rely on rare earths for signal clarity and stability. These sensors are vital in autonomous navigation, object recognition, and situational awareness — key pillars of AI-driven machines.

In data centers and AI infrastructure, rare earths help in cooling systems and high-frequency components that support machine learning algorithms, language models, and high-performance computing. As AI models become more compute-intensive, the demand for rare earths in power-dense and thermally sensitive environments is expected to surge.

This convergence of REEs with AI and robotics positions them as critical enablers of the next industrial revolution, where intelligent machines will augment or replace human labor across logistics, healthcare, manufacturing, agriculture, and defense.

National Security and Defense

The military also leans heavily on REEs for advanced weapon systems, communication equipment, and surveillance technologies:

Samarium-cobalt magnets are used in systems where thermal stability is paramount — such as missile guidance systems, fighter jet engines, and satellite communication arrays.

Technologies like night vision goggles, laser targeting devices, and stealth radar depend on rare earth materials for optical precision, energy efficiency, and electromagnetic resilience.

Autonomous military systems, including unmanned ground vehicles (UGVs) and drones, rely on the same robotics and AI capabilities discussed earlier — again, underpinned by REEs.

As geopolitical tensions rise and warfare becomes increasingly digitized and autonomous, control over rare earth supply chains becomes a direct determinant of defense readiness.

All in all, rare earths are no longer “just another commodity”. Their role in clean energy, AI, robotics, and national defense makes them strategic resources — the backbone of future economic power and military superiority. For that reason, secure access to REEs is non-negotiable.

The Real Rarity: Refining and Processing

As I explained before, despite what their name suggests, REEs are not geologically rare. They are found in significant quantities across the globe — including in the United States, Australia, Canada, Brazil, parts of Africa, and Southeast Asia. However, the real challenge isn’t finding them — it’s refining them.

REEs typically occur in low concentrations and are chemically bound within complex ores, making the process of extraction and separation both technically demanding and cost-prohibitive. Compounding this is the fact that rare earth deposits are often co-located with radioactive elements such as thorium and uranium, which introduces additional regulatory, environmental, and safety hurdles.

The process to isolate usable rare earth oxides involves several stages:

Mining and Crushing: Ore must first be mined and ground into fine particles.

Chemical Leaching and Solvent Extraction: These particles are then subjected to intensive chemical treatments using acidic or alkaline solutions, which dissolve the REEs and separate them from surrounding materials. This step often requires multiple rounds of solvent extraction, an energy-intensive process that uses hazardous reagents.

Separation of Individual Elements: Because REEs are chemically similar, isolating individual elements such as neodymium or dysprosium requires meticulous separation techniques, often using ion-exchange resins or precipitation — both of which generate significant volumes of toxic waste.

Refining into Oxides, Metals, or Alloys: Finally, the purified compounds are converted into the oxides, metals, or magnets used in industrial applications. Each of these steps must meet high purity standards, especially for use in electronics, defense, and medical devices.

The result is a process that is:

Capital-intensive: Developing a vertically integrated REE supply chain, from mine to magnet, requires a huge upfront investment, not to mention years of permitting and construction.

Environmentally sensitive: REE processing has historically led to groundwater contamination, airborne pollutants, and radioactive tailings. In many jurisdictions, these risks have triggered public opposition and stringent environmental reviews.

Politically fraught: The combination of environmental risk, long timelines, and uncertain returns has caused many Western nations to outsource refining capacity, particularly to China — where environmental standards have traditionally been more lenient and industrial policy aggressively supported domestic production.

This strategic offloading has created a global chokepoint: while several countries mine REEs, China controls the vast majority of global processing infrastructure, especially for heavy rare earths — the most critical and difficult to refine.

In effect, the “rarity” of rare earths lies not beneath the ground, but in the infrastructure, expertise, and political will required to refine them. Until alternative refining hubs are built and scaled, the global economy will remain highly vulnerable to supply disruptions, price manipulation, and geopolitical leverage.

China’s Dominance — and the Global Imbalance

Over the past three decades, China has transformed itself into the undisputed leader of the global rare earth industry. While several countries possess rich geological reserves, China’s dominance lies not only in mining but — more critically — in refining, processing, and magnet production, which are the most technologically demanding and strategically valuable segments of the supply chain.

Today, China:

Produces approximately 60% of the world’s rare earth elements

Controls nearly 90% of global REE processing and separation capacity

Handles over 90% of all heavy rare earth refining, which is essential for advanced defense and energy technologies

Manufactures the majority of rare earth-based permanent magnets, which are vital for EV motors, robotics, drones, and military applications

This dominance did not emerge by chance. In the 1980s and early 1990s, the United States was the world’s leading REE producer, anchored by large-scale operations at Mountain Pass in California. Europe, too, had significant processing capabilities, and countries like Australia, India, and Malaysia had active mining programs.

However, beginning in the late 1990s, China began executing a coordinated industrial policy focused on establishing control over the entire REE supply chain. This involved several strategic actions:

Aggressively undercutting global prices by flooding the market with low-cost REEs, driving Western competitors out of business

Offering subsidies and low-interest financing to Chinese companies to expand refining and magnet-making capacity

Relaxing environmental regulations, enabling rapid industrial growth with minimal delays

Consolidating the domestic industry under state-backed giants such as China Northern Rare Earth Group and China Minmetals, allowing for greater policy control and pricing power

Meanwhile, Western nations took a hands-off approach. The U.S. and its allies allowed their rare earth industries to wither, citing high costs, environmental concerns, and a perceived lack of strategic urgency. As a result, critical segments of the supply chain — particularly midstream refining and high-performance magnet production — migrated almost entirely to China.

This has created a global imbalance with serious geopolitical and economic implications. Today, even when countries like the U.S. or Australia mine rare earths, they often export raw concentrate to China for processing, because no comparable refining infrastructure exists domestically. This not only exposes nations to supply disruptions but also limits their ability to capture value from the rare earth economy.

Moreover, China has demonstrated a willingness to leverage its REE dominance as a geopolitical tool. Notably:

In 2010, it cut off rare earth exports to Japan during a territorial dispute in the East China Sea.

In 2023 and 2024, it implemented non-automatic export licensing systems for critical REEs and related products like permanent magnets — providing Beijing with selective control over outbound supply without enacting full bans.

Recently, in response to U.S. tariffs, China has imposed restrictions on the exports of seven rare earth minerals, along with other products, including permanent magnets.

These moves often coincide with trade tensions, military escalations, or strategic negotiations — serving as a quiet but potent form of economic coercion.

As geopolitical competition intensifies, the strategic cost of outsourcing REE refinement to a single country is becoming unsustainable.

The U.S. Dilemma: Rich in Resources, Weak in Processing

The United States is fortunate to possess significant rare earth element (REE) reserves, particularly at the Mountain Pass mine in California, which is currently the only active REE mine in the U.S. Additionally, there are other known reserves in states such as Wyoming, Texas, and Alaska, as well as the potential for offshore deposits. However, despite these abundant resources, the U.S. remains highly dependent on China — not for the raw materials themselves, but for the critical step of refining and processing those materials into usable forms.

Currently, the United States has no operational infrastructure capable of refining rare earth elements to the extent needed for industrial and military applications. Most of the REEs mined in the U.S. are sent to China, where they are separated, refined, and converted into high-value products, such as permanent magnets, batteries, and catalysts. This results in a dependency loop, where the U.S. extracts the raw material but relies on China for the downstream processing that provides the full economic and strategic value.

This vulnerability has become increasingly apparent as geopolitical tensions with China escalate. The Department of Defense and various U.S. policymakers have recognized that securing access to critical rare earths is not just a matter of economic competitiveness — it’s a matter of national security. Many key technologies depend on rare earths, making the U.S. reliance on foreign supply chains particularly concerning.

Toward a “Mine-to-Magnet” Strategy: Rebuilding America's Rare Earth Independence

In response to its heavy reliance on China for rare earth elements, the United States has begun a concerted effort to rebuild a domestic supply chain capable of supporting both its defense and clean energy sectors. Central to this strategy is the U.S. government's use of the Defense Production Act, which since 2020 has directed more than $400M toward enhancing domestic mining, refining, and magnet manufacturing capacity. The goal is to ensure that the nation can produce, process, and fabricate the critical components needed for everything from electric vehicles to advanced weapons systems — without depending on Chinese infrastructure.

Among the key players in this movement is MP Materials (MP), the largest rare earth mining company in the U.S., which has revived operations at the Mountain Pass mine in California. MP is actively working to restore domestic refining capabilities and build a fully integrated operation that spans extraction to end-product manufacturing. Additional projects are underway in Texas and Canada, focusing on building rare earth separation plants and magnet production facilities. At the same time, the U.S. is forging bilateral trade agreements with nations like Australia, South Africa, Brazil, and Greenland (a sensitive topic) to secure access to alternative rare earth supplies. These partnerships are crucial as the U.S. seeks to diversify and de-risk its rare earth sourcing beyond China.

Challenges

Despite this momentum, developing a self-sufficient rare earth ecosystem presents formidable challenges. Building out refining and processing infrastructure demands massive capital investment, with costs potentially reaching into the billions. Creating domestic capacity to manufacture complex end-products like permanent magnets requires not only funding, but also advanced engineering, skilled labor, and long-term policy support. Environmental and regulatory hurdles also loom large. Rare earth mining and refining are resource- and waste-intensive operations, often facing local opposition due to concerns over pollution and land use. Ensuring these projects meet modern environmental standards while remaining economically viable will require coordinated federal and state-level oversight.

Political sensitivities further complicate the landscape. Many prospective mining and processing sites—particularly in remote or environmentally sensitive regions like Alaska, Greenland, and parts of Africa — require negotiation with indigenous groups and local governments. Gaining the necessary approvals and community support could delay or derail critical projects, especially in jurisdictions with strong environmental advocacy movements.

The Goal by 2027

Despite these obstacles, the U.S. has outlined a bold objective: the development of a fully integrated “mine-to-magnet” rare earth supply chain by 2027. This strategy aims to secure control over every stage of the process, from raw material extraction to the final production of magnets used in applications ranging from F-35 fighter jets to wind turbines and EV motors. The Department of Defense has emphasized this timeline as a national security imperative, warning that continued dependence on China leaves the U.S. vulnerable to supply disruptions, geopolitical leverage, and technological stagnation.

Realizing this vision will require more than just investment — it will demand industrial coordination, policy clarity, technological innovation, and international collaboration. The U.S. remains significantly behind China in both refining capacity and expertise in advanced materials processing. Even MP Materials, despite its progress, currently sends some of its mined output to China for final-stage processing. Achieving full self-sufficiency means not only scaling up operations but also mastering the complex science behind producing high-performance magnets and other critical rare earth components.

The next several years will be crucial. Whether the U.S. can transition from ambition to execution will determine its resilience in a world where access to strategic resources is increasingly tied to economic strength and national security. Rare earth independence is no longer just an industrial goal — it is a cornerstone of 21st-century geopolitical strategy.

Final Thoughts

Rare earth elements may be misnamed — they're not rare in nature — but they are unquestionably rare in the global economy, where refined supply is concentrated in just one country. As the world transitions toward electrification, digitization, and rearmament, REEs are poised to become the next critical battleground in the 21st-century resource race.

China’s near-monopoly gives it outsize influence, and its recent moves suggest a willingness to weaponize that dominance. Meanwhile, the U.S. and its allies are scrambling to catch up, racing to secure stable, transparent, and sustainable alternatives.

In this high-stakes environment, rare earths are no longer just technical commodities — they’re a strategic currency in a new era of geopolitical competition.

That’s it. Thanks for reading!

Stay tuned for an upcoming Deep Dive on MP Materials — where I’ll break down the company’s role in reshaping America’s rare earth supply chain.

Be sure to subscribe so you don’t miss it.

Important Communication:

Starting May 1, I’ll start restricting part of my content to paid subscribers. As such, the current price (which was set lower on purpose, since it was voluntary) will change. If you choose to support me before then, you’ll get a 50% discount on the yearly plan. I spend countless hours working to bring you the best content I can, so I appreciate your understanding. Don’t worry — I’ll still publish plenty of free articles as well.

I did my PhD in physics on rare-earth elements. It's true that they're used in quite a number of applications and that China took over the global rare-earth market. Researchers are striving for new types of permanent magnets that don't contain rare-earth elements to reduce the dependence on China. It's a tough call. Some compounds have comparable properties in limited temperature ranges (either very low or very high), so there's no replacement yet. I kind of understand what the US wants from Ukraine with respect to the deal they've been pushing.

Great content! Easy to digest despite the complex topic.