Tempus AI (TEM): Investment Thesis Explained 2.0

Roughly three months ago, I published my first Deep Dive on Tempus AI (TEM).

Since then, several developments have emerged that could act as catalysts for the business.

It’s time to revisit the thesis and introduce a Valuation Model to assess whether TEM is an attractive investment from my perspective.

Introduction

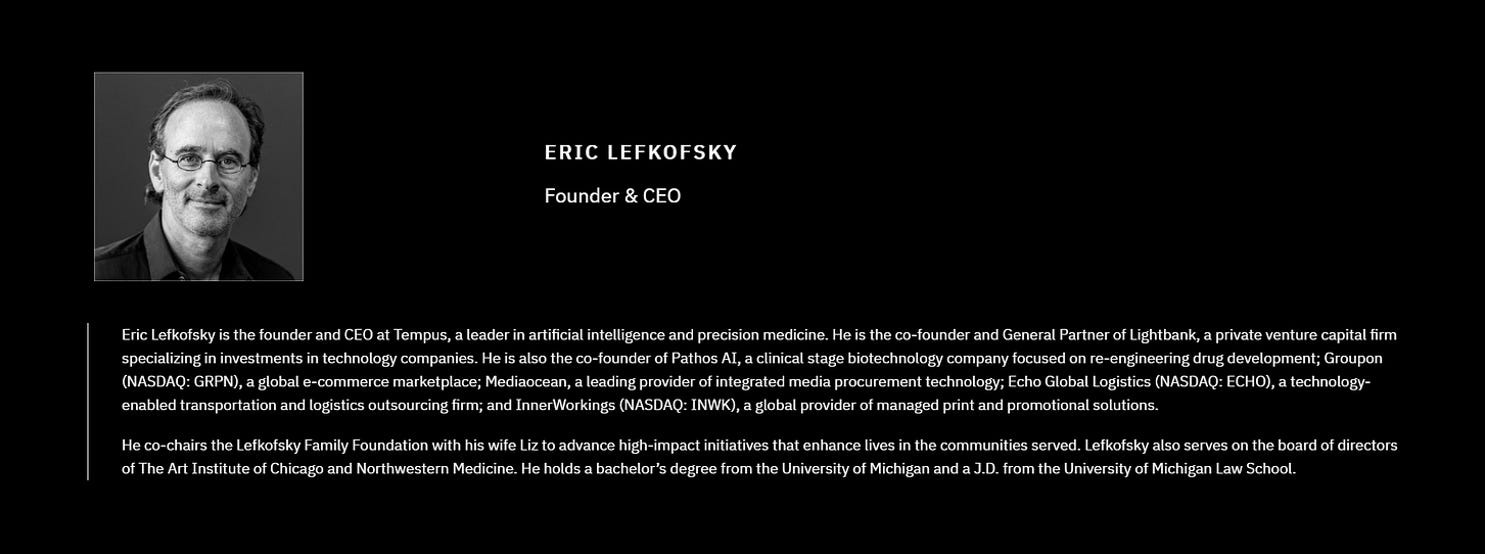

Tempus AI is a cutting-edge precision medicine company founded in 2015 by Eric Lefkofsky. The inspiration for Tempus arose from Lefkofsky’s personal life — his wife’s battle with breast cancer revealed how limited the role of technology was in shaping her care. Determined to change this, Lefkofsky set out to integrate advanced technology into healthcare, addressing a critical gap in the industry.

At its core, TEM leverages AI to analyze vast amounts of clinical, imaging and molecular data. Its goal is ambitious yet clear: to revolutionize healthcare by enabling personalized treatment decisions, advancing drug discovery, and facilitating earlier and more accurate disease diagnoses.

Tempus AI initially focused only on oncology, enabling doctors to deliver tailored treatments for cancer patients. This “intelligent diagnostics” model proved so effective that the company expanded its efforts into other critical areas, such as neuropsychology and cardiology.

Today, TEM’s technology empowers thousands of physicians and life science companies, making a tangible difference in patients' lives.

The Booming Market for AI in Healthcare

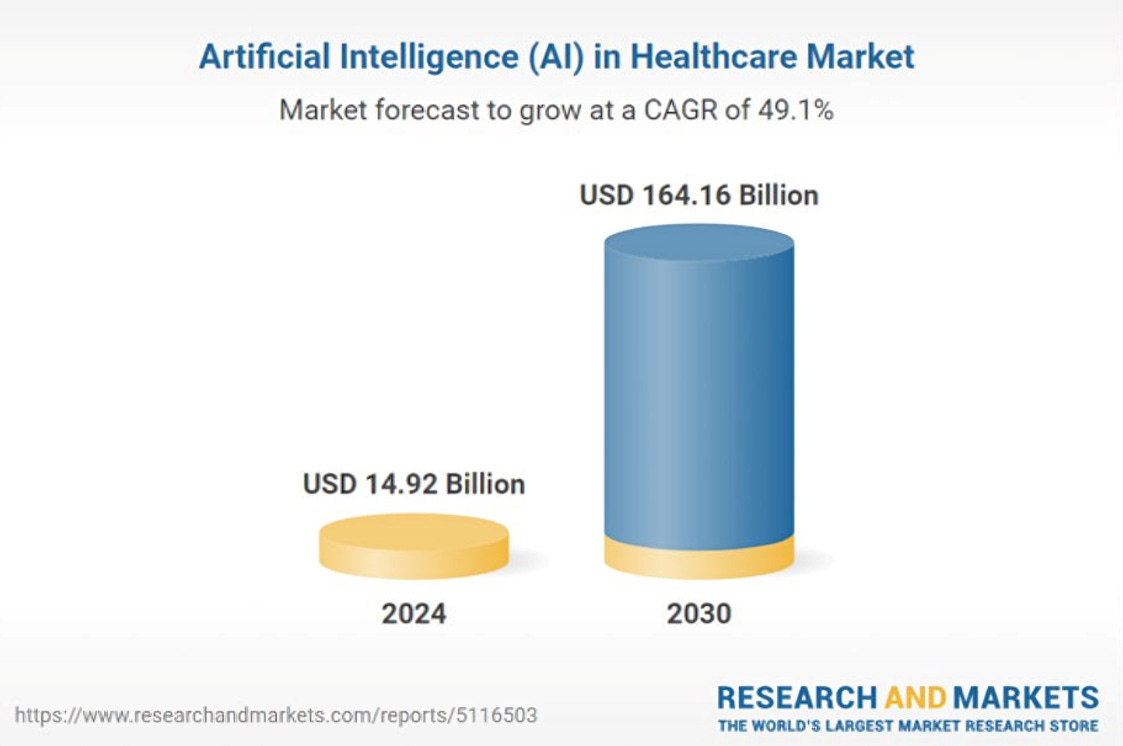

The global AI in healthcare market is experiencing unprecedented growth, projected to expand from $15B in 2024 to a staggering $164B by 2030, representing a CAGR of 49.1%.

This explosive growth is driven by several factors, including:

• Increased Investments: Significant public and private sector funding is accelerating the adoption of AI technologies in healthcare.

• Rapid AI Proliferation: The integration of AI into healthcare systems is transforming diagnostics, treatment planning, and patient outcomes.

• Focus on Human-Aware AI Systems: Advances in AI technology are enabling more personalized and human-centered solutions, which are crucial in the healthcare domain.

Tempus AI is uniquely positioned to capitalize on some of these trends. With its AI-powered precision medicine platform, TEM is not only a pioneer in embedding AI into healthcare workflows but also a leader in driving real-world impact.

How Does Tempus AI Make Money?

TEM operates a highly integrated and scalable business model built on three primary product lines: Genomics, Data Licensing, and AI Applications. These segments are interconnected, creating a "closed-loop" system where each reinforces the others, driving network effects and long-term sustainability.

Here’s how they work:

1) Genomics

Tempus AI runs advanced diagnostic tests, including Next Generation Sequencing (NGS), PCR profiling, and molecular genotyping, for healthcare providers, pharmaceutical companies, and researchers.

• These tests generate molecular and clinical data, which is structured and de-identified before being added to TEM’s proprietary database.

• Revenue is derived from insurance reimbursements or direct payments for these tests.

2) Data Licensing

The data collected from Genomics tests is commercialized through licensing agreements with pharmaceutical and biotechnology companies.

• De-identified, multimodal records: Tempus licenses this database to partners, enabling them to drive drug discovery and development.

The value proposition is clear: by providing real-world data across the full spectrum of drug development — from preclinical discovery to target population optimization or clinical trial design — Tempus helps customers accelerate timelines and improve success rates.

3) AI Applications

In addition to providing the data, Tempus leverages AI to develop practical tools that enhance patient care and optimize treatment outcomes.

Insights and Trials

Actionable Insights: Tempus provides analytical tools that transform raw data into meaningful insights, enabling better decision-making for healthcare providers.

Clinical Trial Matching: The company’s AI-driven platform efficiently matches patients with suitable clinical trials, accelerating the trial activation process to approximately two weeks (vs. typically 6-12 months). This capability is a significant advantage for pharmaceutical and biotech companies looking to expedite their research and development processes.

Clinical Decision Support

Tempus offers AI-driven diagnostics and clinical decision support tools that help healthcare providers deliver more effective and personalized treatment plans. These tools are integrated into Electronic Health Records (EHRs), making them easily accessible and usable within existing healthcare workflows.

With approximately 3,000 healthcare institutions connected to its platform, Tempus has a broad reach and significant market potential. Its ability to integrate with any EHR system further enhances the potential of its market penetration.

The Closed-Loop Advantage

TEM’s business model thrives on network effects:

• The more patients Tempus sequences, the more data it collects.

• This additional data enhances its insights, boosting the value of its Data and AI Applications segments.

• In turn, these improvements attract more partners and providers, driving further adoption of its Genomics services.

This closed-loop system not only compounds the value of TEM’s offerings but also enables sustainable investment into its platform, creating a competitive moat.

TEM’s platform breaks down data silos in healthcare, connecting stakeholders — including physicians, diagnostic companies, and life science firms — through seamless data integration. By enabling data-driven decisions and facilitating collaboration, Tempus creates value at every step of the healthcare ecosystem, ensuring multiple monetization opportunities.

Each of these segments complements the others, forming a cohesive and scalable strategy to bring AI to healthcare at scale.

Let’s address each revenue source in more detail.

Genomics

TEM’s Genomics segment is at the core of its platform, delivering AI-enabled diagnostic tests that are not only smarter but also highly personalized.

These tests integrate contextualized results by leveraging clinical, molecular, and other data modalities, creating a truly intelligent diagnostic.

What Sets Tempus’ Diagnostics Apart?

• Contextualized Results: Tempus combines molecular profiling with clinical data, offering results tailored to the patient’s unique circumstances.

• Patient Comparisons: The company can analyze how similar patients responded to various treatments, enabling personalized care.

• Clinical Trial Matching: Its AI algorithms match patients to trials based on detailed inclusion and exclusion criteria, ensuring precision and speed.

• Algorithmic Insights: Tempus refines therapy selection by embedding purely AI-driven insights, making diagnostics far more actionable.

While a standard diagnostic provides raw results, an intelligent diagnostic knows who the patient is, their medical history, their previous treatments, and how they responded. This allows it to recontextualize findings, offering precision that traditional tests cannot achieve.

Financial Metrics

The Genomics segment grew 24.4% YoY in 2024, with gross margins around 46%.

Last year, this segment accounted for 65% of TEM’s revenue, but in 2025 it'll likely be a larger portion because of Ambry Genetics' acquisition (check next section).

Pricing Power: The price per test is gradually increasing, showcasing TEM’s ability to deliver value and command higher rates over time.

Ambry Genetics Acquisition

In a move to strengthen its genomics segment and broaden its capabilities, Tempus AI recently acquired Ambry Genetics for $375M in cash and $225M in shares. This acquisition marks a strategic step in TEM’s journey to enhance its offerings, expand its footprint, and accelerate its path to profitability.

The acquisition of Ambry brings significant synergies across several dimensions:

• Hereditary Cancer Screening: Tempus has already been using Ambry as a supplier for its germline sequencing (xG) services, which assess inherited cancer risk. With this acquisition, TEM can integrate and expand hereditary risk screening for cancer patients, further enhancing its capabilities.

• Data and Analytics Augmentation: Ambry sequences ~400,000 patients annually, generating a wealth of data. By combining this with TEM’s existing datasets, the company can unlock deeper insights and bolster its data-driven offerings.

• Expansion into New Disease Areas: Ambry’s diverse product line enables Tempus to immediately enter additional categories, including pediatrics, rare diseases, cardiology, reproductive health, immunology, and more.

• Geographic Expansion: With significant lab facilities on the West Coast, Ambry adds valuable infrastructure to TEM’s network, increasing its operational footprint and improving service efficiency.

The Path to Profitability

This acquisition is not just about expanding capabilities, it’s a critical step toward financial sustainability. According to TEM’s Founder & CEO, the combined entity is projected to be both EBITDA and FCF by 2025.

This milestone will mark a significant shift for Tempus AI, validating its business model and long-term strategy.

The Ambry acquisition complements TEM’s closed-loop system, adding new dimensions to its genomics and data capabilities. It positions the company to lead not only in oncology but also in a range of other disease areas, enabling it to serve a broader spectrum of patients and healthcare providers.

Data & Services: Licensing and AI Applications

TEM’s Data & Services segment represents a high-margin, fast-growing revenue source that is poised to play an increasingly critical role in the company’s future.

This segment focuses on licensing its extensive libraries of de-identified clinical, molecular, and imaging data, alongside providing advanced analytics and AI tools to pharmaceutical and biotechnology companies.

What Makes Tempus’ Data Offering Unique?

• Largest Data Library: Tempus has the world’s most comprehensive collection of clinical, imaging, and molecular data. There are ~19M cancer patients in the U.S., TEM has 8.5M cases fully digested and 11M with collected data ready for analysis.

• Key Partnerships: Tempus collaborates with 19 of the 20 largest public pharmaceutical companies, highlighting its importance to the industry.

• Powerful Platform Tools: The company doesn’t just license data — it provides a platform for analysis. Its suite of analytic, cloud, and compute tools enables pharmaceutical companies to derive actionable insights from the data.

Financial Metrics

The Data & Services segment has become a significant driver of Tempus’s growth. It grew 43.2% in 2024, with gross margins around 71.5%.

• Contracts in Hand: As of Q1 2024, Tempus has signed contracts with a total remaining value exceeding $940M, with the majority expected to be realized over the next several years.

• Customer Retention: Tempus’s ability to deepen relationships with customers is reflected in its Net Revenue Retention (NRR): 125% in 2023, increasing to 140% in 2024. Customers often progress from licensing discrete datasets to signing multi-year strategic collaborations, showcasing TEM’s value and indispensability.

The Power of a Connected Platform

TEM’s platform amplifies the value of its data through its integration with the healthcare ecosystem:

• Bidirectional Data Flow: Tempus’s “data pipes” connect with over 2,500 institutions, enabling the seamless flow of information from hospitals to TEM and back, with actionable insights delivered in days.

• Network Effects: With over 65% of Academic Medical Centers and 50% of oncologists in the U.S. using TEM’s platform, its ecosystem continues to expand, enhancing the quality and breadth of its datasets.

The combination of unparalleled data resources, cutting-edge AI tools, and strong partnerships positions Tempus as a leader in this high-margin sector. As Data & Services scales, it is expected to drive significant operating leverage and profitability for the company, ensuring its importance in the future of precision medicine and drug discovery.

Tempus’ leadership in this segment was recently reinforced by the announcement of expanded strategic collaborations with AstraZeneca and Pathos AI.

These multi-year agreements aim to co-develop what is expected to be the largest multimodal AI foundation model in oncology, leveraging Tempus’ uniquely rich library of de-identified oncology data. The initiative will integrate biological and clinical insights to help accelerate the discovery of new drug targets and therapies, and Tempus is set to receive $200M in licensing and model development fees as part of the deal.

This milestone not only validates the strategic importance of Tempus’ data moat but also demonstrates the scalability of its platform in shaping the future of precision medicine. As the foundational AI model is built and adopted globally, it should serve as both a technical and financial catalyst for the company over the coming years.

Additionally, the company recently announced the acquisition of Deep 6 AI, a leading AI-powered platform that helps match patients to clinical trials by analyzing both structured and unstructured EMR data in real time. With integrations across 750+ provider sites and access to over 30M patients, Deep 6 will significantly expand Tempus' existing network.

AI Applications Is A "Nascent" Product Line

While Tempus is viewed as a leader in integrating AI into healthcare, its AI Applications product line is still in its early days.

This segment, which focuses on algorithmic diagnostics and clinical decision support tools, is currently reported within the broader Data & Services category due to its relatively small contribution to revenue.

Its flagship platform, “Next”, is a machine learning-powered system designed to identify gaps in patient care — initially for oncology and cardiology — by analyzing routine clinical data (labs, genomics, imaging, clinical notes).

The strategic intent behind “Next” is to surface at-risk patients earlier in their disease progression, enabling earlier interventions and more effective treatments. Over time, Tempus plans to enhance this platform using LLMs and generative AI, capitalizing on its proprietary dataset of de-identified clinical and molecular information.

Tempus develops these diagnostic algorithms (“Algos”) via three pathways:

Internally, using its extensive data repository;

In collaboration with third parties;

Via licensing of externally developed algorithms.

Once an Algo is validated clinically, it's commercialized through Tempus’ existing infrastructure. This includes its Genomics salesforce, EHR integrations, requisition forms, and online portals — enabling clinicians to order both molecular tests and AI diagnostics from a single vendor using a single patient sample.

Example: The company’s HRD (homologous recombination deficiency) and TO (tumor origin) algorithms in oncology are already integrated into daily clinical workflows.

Tempus is also developing algorithms based on traditional pathology tools (e.g., IHC and H&E staining), which can help identify candidates for therapies or clinical trials that might otherwise go unnoticed.

Commercialization model:

Revenue depends on whether each Algo can be billed to payers.

At launch, most Algos face limited reimbursement.

Over time, Tempus expects reimbursement rates to improve as it builds clinical evidence and demonstrates utility. This would be a huge catalyst for the company.

Current Numbers

• 2024 Revenue: $12.4M (1.8% of total revenue)

• 2023 Revenue: $5.5M (1.0% of total revenue)

• 2022 Revenue: $1.4M (0.4% of total revenue)

Gross margins: “north of 85%”

AI Applications represent a significant long-term opportunity, potentially transforming how diagnostics are delivered and expanding the company’s TAM. The company is actively developing additional algorithms, which, if successful, could drive exponential growth in this segment.

Tempus has been methodically laying the groundwork for AI Applications by building a strong moat: The World's Largest Dataset + Expanding Network Effects.

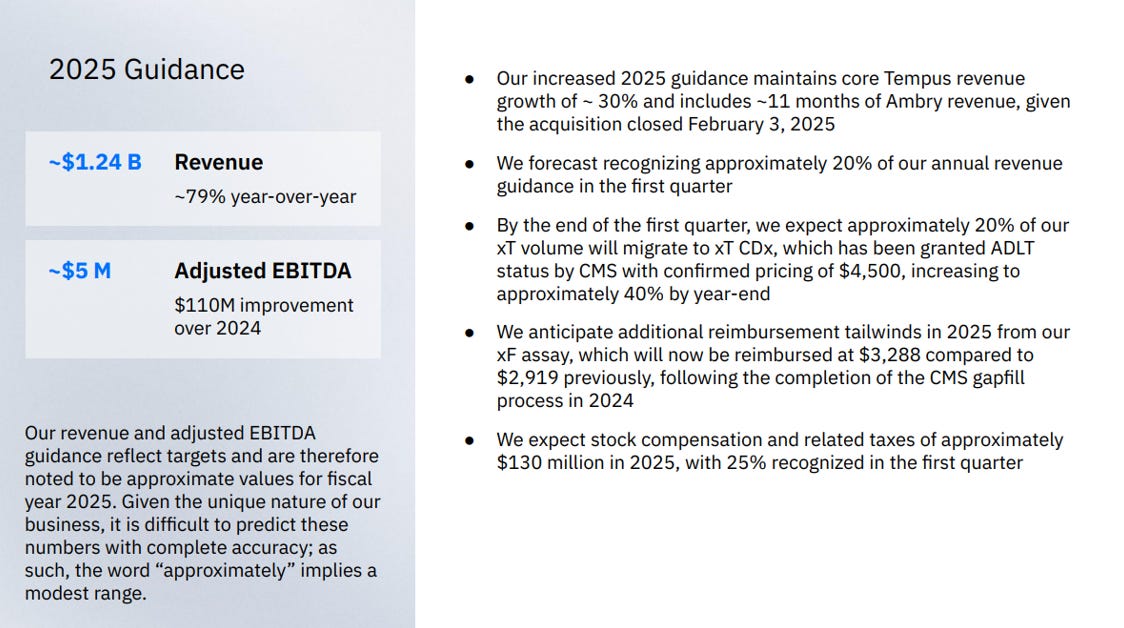

Outlook for 2025

• Revenue to be ~$1.24B, growing by 79% YoY

• Adj. EBITDA to be ~$5M and FCF to be positive

One point worth noting about the 79% YoY revenue growth guidance for this year: In 2024, the combined entity of Tempus and Ambry Genetics generated close to $1B in sales. Therefore, the organic growth projected for 2025 is about 30%.

While this is still strong, especially considering it’s coupled with operating leverage, it’s not as impressive as it may initially appear.

Valuation Model

When I published my first Deep Dive on Tempus AI, this was my conclusion on its valuation:

“Essentially, I don’t think TEM is a clear bargain at these levels based on its current numbers, but I also believe that if the company proves it can execute on its mission, then a $5.5B market cap will eventually be seen as mere nickels for such a valuable and life-saving ecosystem.”

In this update, I’m building a new valuation model to value each segment of the company separately before aggregating them into a Sum-of-Parts valuation.

I must say: Tempus AI is a very challenging business to value, but I’ll do my best to make reasonable assumptions.

Let’s start with Genomics.

Tempus’ guidance implies that Ambry Genetics will contribute roughly $324M in revenue in 2025. I'll include that entirely within the Genomics segment.

Assuming a 15% CAGR through 2030, this segment would reach ~$1.7B in revenue by then.

As discussed, the gross margin for this segment was 46% last year, slightly down from 47.9% YoY.

These are the only three pure-play genomics companies listed on the stock market that Tempus AI considers competitors in this segment: Guardant Health (GH), Natera (NTRA), and NeoGenomics (NEO).

Based on these peers and other more mature companies in related spaces, it's reasonable to assume that at a $1.7B scale, Tempus could achieve at least 55% gross margins and 10–20% FCF margins. Let’s use the midpoint: 15% FCF margin.

That would imply around $255M in FCF by 2030.

In my view, this is the segment that deserves the lowest valuation multiple. Given that most genomics companies aren’t FCF-positive yet, it’s difficult to find a perfect proxy — but I'll use a 20x FCF multiple as a reasonable benchmark.

This results in a $5.1B valuation for the Genomics segment by 2030, which discounted at 10% implies a present value of ~$3.48B by 2025YE.

Now, let’s value the Data Licensing segment.

Tempus management recently noted that the NRR of 140% should be viewed as a peak, and that accelerating beyond this will be difficult. However, demand for high-quality healthcare data continues to increase as the world shifts toward AI-driven healthcare solutions.

Assuming a 25% CAGR through 2030, the Data Licensing segment (excluding AI Applications) would reach ~$874M in revenue.

Gross margins for this segment were 71.5% last year, up from 66.5% YoY.

This business is high-margin, scalable, and behaves more like a software platform. I believe it could reach 80% gross margins and around 25% FCF margins by 2030, leading to $218.5M in FCF.

Given the quality of the business model, I think a 25x FCF multiple is appropriate and could even be considered too low.

This results in a $5.5B valuation for the Data Licensing segment by 2030, and a present value of ~$3.73B by 2025YE.

And finally, let’s value the nascent line of AI Applications.

This one is even trickier.

At the 24th Annual Needham Virtual Healthcare Conference, management indicated that this business line has "north of 85% gross margins."

Due to the nature of the business, I think 35% FCF margins are very achievable, potentially even higher.

Given its small size today (and recent trends), I’m assuming 50% CAGR through 2030, which would bring it to $141M in revenue and $49.4M in FCF.

Considering the margin profile and market sentiment around AI, a 35x FCF multiple seems fair — although by 2030 it could arguably be even higher, just look at comparable companies (not necessarily within healthcare, but AI-related and with similar profiles). I try to stay conservative, and I’m already stretching a bit here.

This results in a $1.73B valuation for the AI Applications segment by 2030, with a present value of ~$1.18B by year-end 2025.

Sum-of-Parts Valuation

Putting it all together:

3.48B + 3.73B + 1.18B = $8.39B

→ ~$48/share.

At current prices, this implies a 10% downside.

And I'm not even accounting for the likely dilution in the coming years.

In short, while I love Tempus AI as a company and strongly support its mission, I don’t believe it offers asymmetric potential at today’s valuation. Even with assumptions that are not really conservative, the intrinsic value I estimate remains slightly below the current market cap.

To be clear, I still think Tempus could generate good returns over the long term. However, from an opportunity cost perspective, I see more attractive investments elsewhere at this time.

Important Reminder: Valuing Tempus AI is extremely challenging — both at the company level and within each segment individually. Many of my assumptions are subjective, but that’s true for every valuation exercise. I typically lean conservative, but going too conservative here would likely be unrealistic due to the attractiveness of this sector for most investors. As I always say: If you need a DCF model to convince yourself a stock is cheap, it’s probably not cheap enough. I use exercises like this to frame possible valuation ranges — not to find artificial precision.

Potential Catalysts

• Institutional Ownership Growth: Institutional investors currently own ~36% of TEM, which is relatively low for a company of its size and growth potential. As more institutions recognize the value of TEM’s platform and its role in the healthcare ecosystem, this number is expected to increase, which could provide a strong catalyst for price appreciation.

• Improving Margins: TEM is approaching an inflection point where its margins are poised to improve significantly. As its high-margin Data Licensing and AI Applications segments scale, and as it integrates Ambry Genetics into its platform, the company should finally see profitability.

• Expansion Beyond Oncology: TEM has already made strides in expanding its reach beyond oncology into areas like neuropsychology, cardiology, and rare diseases, opening up new revenue streams. With its robust platform, Tempus is well-positioned to make further inroads into additional healthcare areas.

• Potential Reimbursement for AI Applications: One of the most exciting catalysts for TEM’s growth in the long term lies in the future reimbursement of its AI applications. As regulators begin to recognize the tremendous potential of AI to improve patient outcomes, TEM’s AI-driven diagnostics and decision-support tools could qualify for reimbursement, providing a major revenue boost. The CEO is optimistic about this potential, and if realized, it could become a significant driver of growth. However, it’s worth noting that this will likely take several years to materialize.

• (NEW) Regulatory Tailwinds from FDA’s AI Shift: The FDA’s recent move to embrace AI-based computational modeling as a replacement for animal testing marks a major turning point in drug development — and a huge opportunity for Tempus. The company’s extensive clinical and molecular dataset, combined with its advanced AI infrastructure, directly aligns with this new framework. With the FDA now validating AI-powered models as part of the drug approval process, Tempus is in a prime position to become a critical partner for pharmaceutical companies seeking faster, more cost-effective paths to market. This shift could significantly expand Tempus’ role in drug discovery and development over the coming years.

Risks to Mention

Execution Risks:

Tempus AI may fail to scale its platform across multiple sectors of healthcare. If the company ends up focusing solely on oncology, growth could be slower than expected.

Although AI applications in healthcare have enormous potential, the adoption of these technologies is still in its early days. There is a risk that Tempus’ AI solutions may face challenges in market acceptance, either due to competition or a slow rate of adoption from healthcare providers.

The AI applications segment is still nascent and subject to fast-changing market dynamics. As the company moves from research to commercialization, there’s a risk that the solutions will not scale as quickly as anticipated, or that competition in AI healthcare will intensify.

Regulatory and Legal Risks:

The healthcare industry is highly regulated, with rules varying across countries. Changes in regulation, particularly around data privacy and AI, could limit Tempus’ ability to scale.

As a company operating at the intersection of healthcare and AI, Tempus could face legal risks associated with the use of its technology. Errors in diagnostic AI could lead to lawsuits or reputational damage, especially if the technology doesn't perform as expected.

Competitive Landscape:

The genomics and AI healthcare sectors are highly competitive, with both established players and new entrants fighting for market share. Companies like Guardant Health, Natera, Roche, and others are not standing still and will continue to innovate. If Tempus fails to maintain a competitive edge in terms of technology, partnerships, or cost structure, it could lose market share.

While Tempus is leveraging AI and genomic data, advancements in alternative technologies (more efficient platforms) could reduce the company’s competitive advantage over time.

Market Sentiment and AI Hype:

Tempus’ stock price could be highly sensitive to shifts in market sentiment around AI in healthcare. As the sector continues to evolve, any slowdown in AI adoption or failure to meet growth expectations could lead to sharp sell-offs, especially if investor enthusiasm around AI-driven healthcare wanes.

Insiders' Alignment

If you follow me, you know that I always look for companies where the Founder is still the CEO and remains the largest individual shareholder. This alignment between the company's leadership and shareholders is crucial for long-term success, as it ensures that management is motivated to drive value for all stakeholders.

At Tempus, Founder and CEO Eric Lefkofsky holds over 20% of the company, demonstrating a strong personal stake in its future. Overall, insiders own ~35% of the company, further aligning their interests with those of shareholders.

Importantly, TEM has two interesting investors: Google and Novo Nordisk. Google owns around 1% of the company, while Novo Nordisk holds 2.5%. These high-caliber investors add credibility to Tempus, reinforcing its position in the healthcare and AI space.

Final Thoughts

Overall, I believe Tempus AI is one of the companies best positioned to benefit from the growing integration of AI into healthcare to improve patient outcomes. The company’s platform is paving the way for personalized, data-driven healthcare solutions, and it stands to capitalize meaningfully on this long-term shift.

I haven’t pulled the trigger at $30/share, as I was hoping for a more attractive valuation. However, with several catalysts on the horizon — and growing awareness of TEM’s potential — that opportunity may never materialize.

In my view, Tempus is a very interesting stock to own as part of a diversified growth portfolio. But in my particular case, it doesn’t fully meet my criteria for asymmetric upside within a 2–5 year timeframe. As a highly concentrated investor, I prefer not to rely on broader AI healthcare hype to deliver outsized returns — even though I do believe TEM could ride that wave successfully.

I’ll continue to closely monitor the company's performance over the coming quarters and years. While I’m not planning to initiate a position at current valuations, after studying Tempus for several months, I’m genuinely fascinated by its long-term prospects and will be watching its execution very carefully.

That’s it! I hope you found this article useful.

Important Communication:

Starting May 1, I’ll restrict part of my content to paid subscribers. As such, the current price (which was set lower on purpose, since it was voluntary) will change. If you choose to support me before then, you’ll get a 50% discount on the yearly plan. I spend countless hours working to bring you the best content I can, so I appreciate your understanding. Don’t worry — I’ll still publish plenty of free articles as well.

I’m also working on adding extra perks to make the subscription even more valuable.

Upcoming Deep Dives: MP and ALVO.

Thank you Manuel for your very thorough review.

I just discussed your latest TEM deep dive with an investor who was long on PLTR since recommending it at $15 (based on a WhatsApp conversation I had with him dated 8/15/23).

He sees strong parallels between TEM and PLTR, believing analysts are currently mispricing TEM just as they initially misjudged PLTR. In his view, applying a 15% earnings growth rate to TEM significantly understates its long-term potential.

He emphasized that with the AI wave expected to reshape the healthcare sector, TEM is uniquely positioned. Unlike many newer entrants, TEM already has the necessary data infrastructure and technology in place, having provided healthcare recommendations long before formally pivoting to AI. This gives TEM a critical first-mover advantage in healthcare AI.

He believes TEM is poised for explosive growth similar to what PLTR experienced — and views the recent pullback, driven by tariff concerns, as a buying opportunity.

Any thoughts on this parallel?

Great thesis on a very interesting company, thanks much!