High Tide (HITI): Q2 FY2025 Earnings Review

High Tide (HITI) just reported its fiscal Q2 2025 results for the three months ended April 30, 2025.

In this article, I break down the key highlights and share where my long-term investment thesis stands today.

Consolidated Numbers

As usual, the best way to assess the company’s performance is by first looking at the consolidated numbers before diving into the segments.

Here’s a quick snapshot of the quarter:

• Revenue of $137.8M vs. $138.5M est. (up 11% YoY, or 12% when adjusting for the one fewer day in this fiscal quarter)

If we go with the 12% YoY growth figure, this marks the fastest growth rate in six quarters — great to see continued acceleration.

• Gross margin of 26% vs. 28% YoY and 25% QoQ

The YoY decline was expected due to the ecommerce business model shift, but it’s encouraging to see margins improving sequentially, driven by strength in the core business.

• Adj. EBITDA of $8.1M vs. $5.9M est. (down 20% YoY, but up 14% QoQ)

This came in better than I expected, especially considering this was the first full quarter reflecting the impact of the ecommerce transition.

• EPS of ($0.04) vs. ($0.03) est.

• FCF of $4.9M vs. $9.4M YoY

It's good to see the company back to generating positive FCF after a ($1.9M) outflow last quarter. Management has consistently guided that FCF will fluctuate quarter to quarter based on store openings.

• Cabana Club members at 1.9M, up 33% YoY

• ELITE members up 120% YoY (5.1% of total members vs. 4.6% QoQ)

• Daily same-store sales were up 6.2% YoY, the fastest growth rate in five quarters

• Market share of 12% vs. 11% QoQ

• Reached 200 stores across Canada, while competitors continue to contract

This is exactly what we want to see—market share resuming its upward trajectory.

The outlook for 2025:

• To open 20-30 new stores organically in Canada

• To remain FCF+ for the entire fiscal year

• To enter the German medical cannabis market

• Continued expansion of white label product offerings

Core Business: Brick-and-Mortar Stores in Canada

High Tide’s core business now accounts for approximately 96.6% of total revenue.

Growth in this segment decelerated from +17.3% last quarter to +15.6% this quarter. However, as previously noted, this was impacted by one fewer day in the fiscal period. It’s still encouraging to see growth holding above the 15% mark — a meaningful acceleration from last year.

Importantly, while last quarter’s strong topline performance came at the expense of margins, this quarter showed sequential improvement:

• Gross margin of 25.5% vs. 24.5%

• Adj. EBITDA margin of 7.6% vs. 6.2%

With the ecommerce segment continuing to weigh on profitability, it’s reassuring to see the core business helping to stabilize overall margins.

On the earnings call, Raj Grover mentioned that margins should improve further in Q3 and shared an important update on the illicit market. While challenges persist in urban areas like Toronto and Ottawa, Raj noted that the situation has at least stabilized:

“It hasn’t changed, but it’s also not gotten worse.”

More encouragingly, in smaller markets — where the illicit presence is minimal — competitor store closures are accelerating. This trend is giving High Tide room to expand margins, just as management had forecasted. Raj emphasized that margin improvement is already underway in these regions and is expected to continue.

I’m also very optimistic about the ramp-up in White Label SKUs, which carry 5–8% higher gross margins on average. Although they currently represent just ~1% of revenue, management appears committed to scaling this category — and the timing couldn’t be better.

The Canadian cannabis supply chain is finally stabilizing after years of oversupply. Inventories are now balanced, pricing has become more predictable, and Canadian LPs are exporting more to Europe, helping absorb excess capacity. This improved environment removes a major obstacle High Tide had faced: previously, by the time a White Label product was ready for launch, the base SKU it was modeled on had already dropped in price.

That’s no longer the case. Brands like Cabana Cannabis Co. and Queen of Bud are gaining traction, and with Canada running tighter on inventory, pricing power may finally return to producers. This shift should allow High Tide to scale its White Label strategy more efficiently and capture stronger margins over the medium term.

• Operating expenses were 22.7% of revenue vs. 22.8% QoQ — a minor improvement, but still meaningful considering this quarter had three fewer days than the prior one.

The next quarter seems to be positioned to be a strong one:

“Q3 is traditionally seasonally a stronger quarter for us, and we have seen that so far through the quarter. Our retail machine keeps rolling on.”

Path to 300+ Stores

High Tide reaffirmed its long-term goal of surpassing 300 stores in Canada. The CEO highlighted an uptick in competitor closures and improved access to top-tier real estate, especially in Ontario and Alberta.

Management noted that all nine stores opened year-to-date were built organically, and another dozen Tier 1 locations are currently under construction — again, all organic. Thanks to its strong brand, High Tide often receives early access to prime locations from major landlords, frequently without facing competitive bids.

While M&A remains a possibility, Raj made it clear that organic growth will continue to take priority. Acquisitions are difficult to justify unless the location is truly strategic, due to High Tide’s strict ROI discipline.

With 82 stores in Ontario and a provincial cap of 150, there remains ample room to grow. Alberta is also a key opportunity, with management targeting 30–40 additional stores in the province.

Overall, High Tide continues to solidify its position as the leading cannabis retailer in Canada. I remain very pleased with the performance of this core segment, especially given the lingering headwinds from the illicit market — which now appear to be stabilizing.

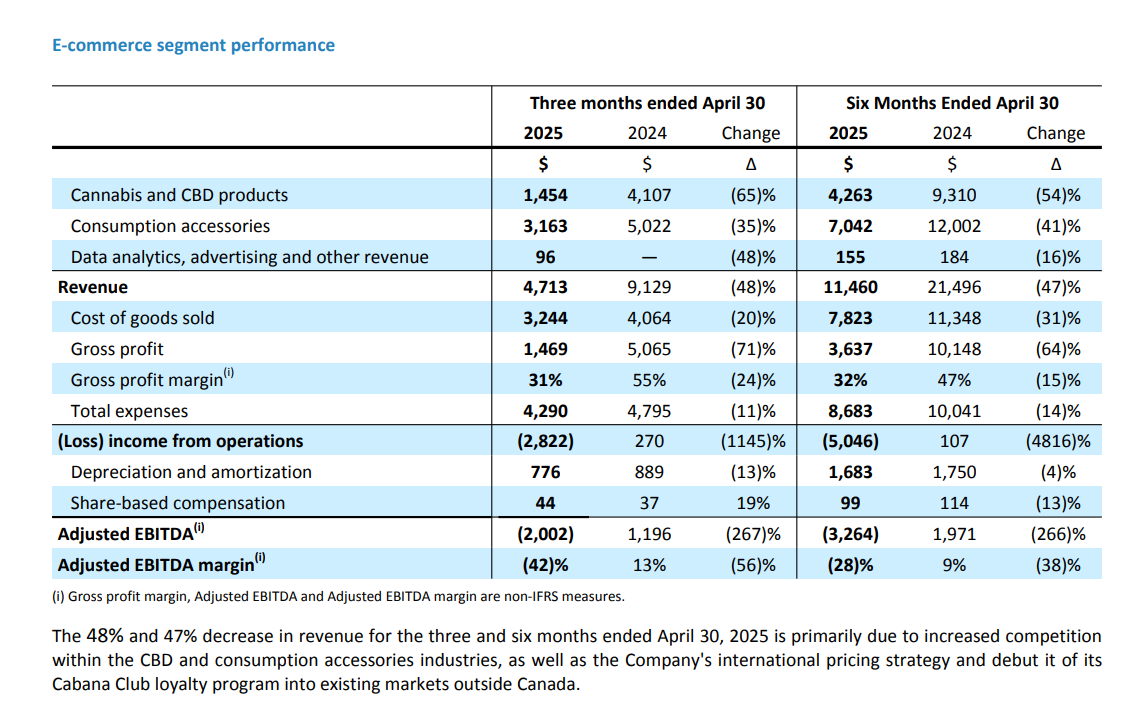

E-commerce Segment: Please Stop Being Stubborn

Although it now contributes just 3.4% of total revenue, the e-commerce segment continues to have an outsized negative impact on High Tide’s consolidated financials.

The image below clearly illustrates just how poorly this side of the business is performing:

Yes, we know the root cause is the business model shift implemented in December 2024 (refer to my Q1 earnings review for full context). The change was intended to revive a segment that has been underperforming for years — but in my view, the strategy simply isn’t working.

Here’s what management said in the press release:

“While the company is currently behind its original revenue expectations, this line item represents an immaterial share of consolidated revenue of just 3%. The company remains committed to its communicated 12-month plan to bolster its e-commerce platforms, which are strategically positioned to take advantage of further federal reforms in the U.S. and elsewhere.”

Frankly, I don’t think it’s fair to brush off poor performance just because the segment represents only 3% of revenue. That may be true — but those 3% managed to wipe out 20% of overall Adj. EBITDA. That’s material.

Second, I question the strategic value of these e-commerce assets in the context of potential U.S. federal reform. Even if reforms were to happen — which remains uncertain after years of delays — these websites don’t have any meaningful traffic or loyal customer base to capitalize on the opportunity. The numbers speak for themselves.

In my opinion, High Tide should divest this segment and reallocate its focus toward the core Canadian retail business and the emerging medical cannabis opportunity in Germany. The company can always retain its U.S. consumer data for future use if and when the regulatory environment shifts.

Reviving this segment has been a costly distraction, and it’s time for management to acknowledge that. Holding onto it in hopes of a future turnaround feels more like stubbornness than strategic thinking.

Fortunately, during the earnings call, Raj Grover said:

“But look, ultimately, we will be completely flexible to do whatever is required to maximize shareholder value, whether that means getting a more leaner structure in our e-commerce divisions, putting them on hold and raising back pricing to just hold them for federal legalization or selling them entirely. Everything is on the table. We're not married to the e-commerce segment, we know what is our core business. That has never changed. That plan has never changed.”

That’s encouraging to hear. Now let’s hope the team follows through — puts pride aside — and makes the right decision for shareholders.

The Entry into the German Medical Cannabis Market

High Tide provided a detailed update on its highly anticipated plans to enter the German medical cannabis market — a key catalyst to unlock meaningful operating leverage. While management had initially hoped to be operational in Germany by now, they emphasized a deliberate decision to adopt a more cautious and thorough approach, given the evolving regulatory landscape and the potential strategic importance of this expansion.

The CEO Raj Grover explained that the original plan — leveraging High Tide’s strong relationships with Canadian licensed producers (LPs) to export into Germany — has become significantly de-risked over the past few months. Rather than having to negotiate favorable terms, many LPs have proactively committed to working with High Tide, with several even offering to partner exclusively in Europe.

With a preferred German partner and transaction terms now identified, the company is awaiting finalization before going live. Supply is already secured, and the business model is fully mapped out — further reinforcing management’s confidence in the execution of this strategy.

As I’ve said before, High Tide holds a clear competitive advantage in this arena. Most of the medical cannabis sold in Germany is imported from Canada, and no company has stronger relationships with Canadian LPs than High Tide — the country’s largest cannabis retailer.

Here’s what Raj had to say:

“We have 40-plus licensed producers that have already confirmed that they would love to do business through us in Europe — so reroute their offerings through us. Many of them actually voluntarily said that they would love to give us exclusivity in Europe for their products because they already do so much business here with us in Canada. And this is not partner-dependent in Germany. I can literally pick any partner that I want to in Germany and nothing changes on the Canadian front.”

This move could become a highly accretive leg of the business over the next several years.

Other Updates

Solid Balance Sheet

Total debt: $25.4M, with no upcoming maturities in the next two years

Leverage: 0.8x TTM Adj. EBITDA

Cash and cash equivalents: $34.7M

High Tide continues to maintain a solid balance sheet, with ample liquidity and conservative leverage. The absence of near-term debt maturities provides flexibility as the company pursues both domestic expansion and its entry into Germany.

Regulatory Landscape in Canada

During the earnings call, Raj Grover reiterated High Tide’s commitment to influencing cannabis policy in Canada, emphasizing the company’s active engagement with all levels of government. The focus remains on advocating for regulatory changes that support licensed retailers and help suppress the still-prevalent illicit market.

One recent win came out of Manitoba, where new regulations restrict cannabis licenses for gas stations and convenience stores to smaller communities. This was a welcome development for High Tide, which has had a strong footprint in the province since the early days. As Raj pointed out, the previous policy not only disadvantaged established retailers but also failed to adequately protect youth, who often visit those locations with family.

Grover also highlighted Ontario’s recent decision to remove outdated restrictions on in-store product visibility — a change that follows similar moves in British Columbia, Manitoba, and Alberta. These regulatory updates should enhance the customer experience and give legal operators a better chance to compete with unlicensed sellers.

Looking ahead, High Tide remains “especially engaged” with Alberta and Ontario, its two largest provincial markets, as both continue to explore additional measures to level the playing field.

While it’s unclear whether the new Prime Minister’s fall budget will include cannabis-related policy changes, it’s clear that High Tide is taking a proactive role in shaping a more competitive and responsible regulatory environment across Canada.

Final Thoughts

Heading into this quarter, I was concerned it could be a rough one, given that it was the first full quarter reflecting the impact of the e-commerce segment’s business model shift. Fortunately, the results came in better than I expected.

It’s encouraging to see the core business continue to perform well, delivering solid growth and margin expansion even amid broader market headwinds. It’s also reassuring to hear management seriously considering a divestiture of the e-commerce segment, which in my view is long overdue.

Equally important, the German expansion plans are clearly back on track, with LP partnerships already in place and the business model mapped out. If management executes well — divesting the underperforming assets and ramping up the German medical opportunity — 2025 could become a transformative year for High Tide. That includes real potential for operating leverage and growth acceleration, two critical ingredients to drive a meaningful re-rating in valuation multiples.

I’m not currently adding to my position (just over 9% of my portfolio as of the last update), as I don’t expect near-term momentum in the broader cannabis sector and still want to see more clarity on the Germany rollout. That said, I’m far more comfortable with it now and have no intention of selling. At today’s valuation, HITI remains incredibly cheap, and I remain confident that the future is bright for the company.

Disclaimer: As of writing, M. V. Cunha holds a position in High Tide (HITI) at $1.69/share.

Thanks for reading!